As a parent, we always try our best to do the best for our children. It is so natural to want to provide everything we can for our children and to want them to have a happy and carefree life.

When it comes to a child’s financial future after your retirement, parents easily fall into stress. But fret not, here are five things you can do now to ensure that your child’s financial futures are secure.

1. Start Saving Early

The first thing to do if you want to ensure you will have enough money to live comfortably during retirement is to start saving early, according to an expert. The longer you save and the more you invest earlier in life, the more money you’ll have when you retire.

Then you don’t have to worry about being in debt and becoming a burden on your children once you retire. You can ensure that you have enough to live a comfortable life and perhaps even help out your children from time to time.

Furthermore, you can encourage your child to start saving as soon as they are earning money themselves. You can also encourage them to start a side hustle. A side hustle is a part-time job that earns extra money to help your child save for the future.

The sooner you encourage your child to start saving, the more time you’ll have to help them get into a good savings habit. There is nothing worse than wanting to save money but not having the discipline to put it away.

2. Pay Off Debt

Debt is bad for your bank account and it’s an unproductive way of using money. Working towards paying off debt as soon as possible is a great way to both save money and improve your credit score.

If you have credit card debt, make every effort to pay it off as soon as possible. Even if that means being charged more for insurance and rental applications, you will save yourself a lot of trouble later on in life.

Nearly every card allows you to pay off smaller amounts over time and minimize your payments. It’s definitely worth it to pay a little extra each month to pay off debt as quickly as possible.

Pay all the debt before you plan for retirement. This will free up cash flow so you can put away more money each month. You should consider refinancing your loan while rates are still low if you know you will need a loan in the future. This will likely save you money in interest over the life of your loan.

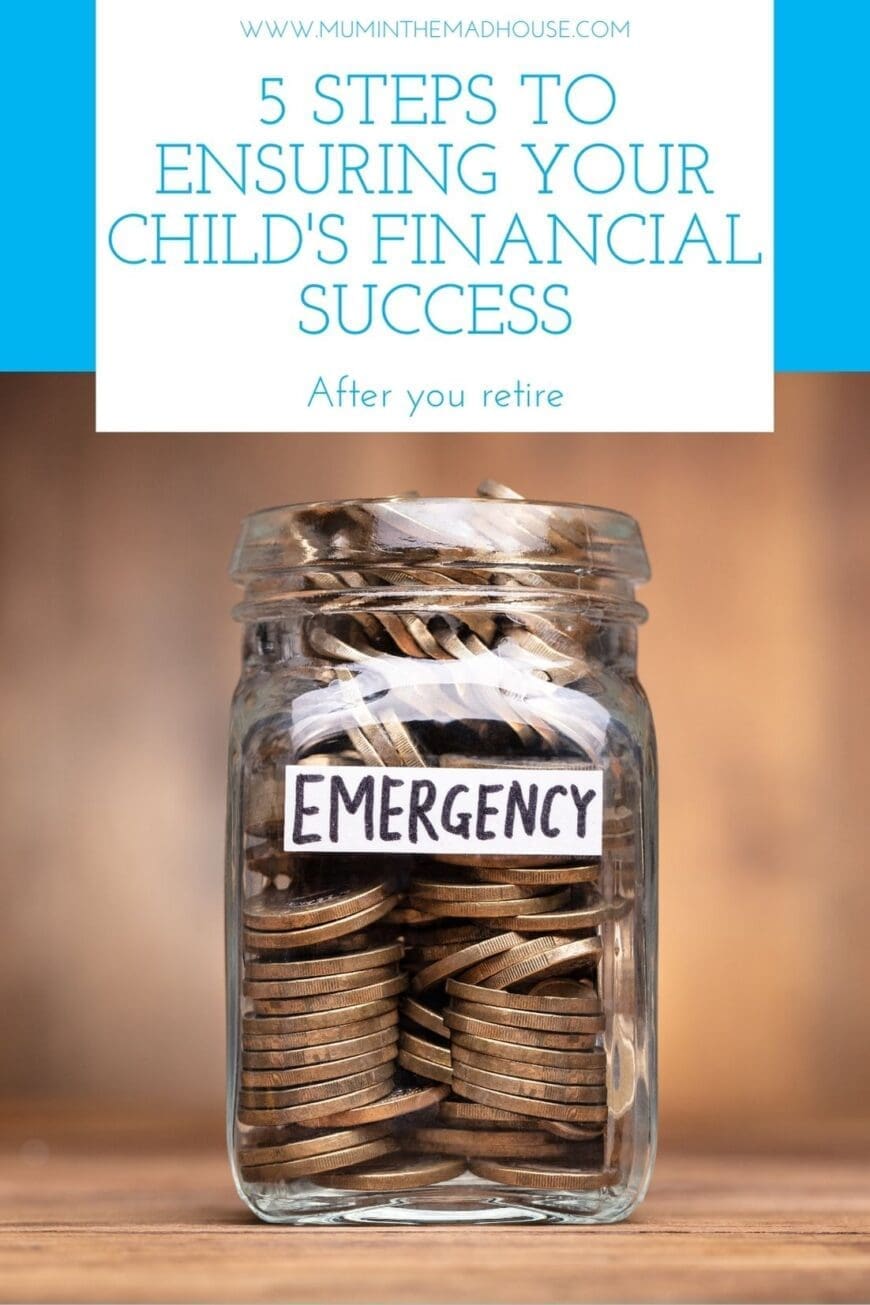

3. Set Up an Emergency Fund

Disasters happen. Nobody ever expects a fire, hurricane, tornado, or another natural disaster, but every year there are natural disasters that cause damage to property and leave people struggling to recover.

The best way to take care of your beneficiaries from these types of events is to set up an emergency fund, perhaps one that your children can inherit if you don’t end up needing it in your lifetime.

An emergency fund is money that you save for unexpected events, like a car breaking down, a medical issue, or a lost job.

It’s important to remember that an emergency fund is not meant to be used for everyday expenses. It should only be used for things that are not covered by your regular budget.

For example, you shouldn’t use your emergency fund to fix a leaky faucet or pay for everyday expenses like utilities or groceries. An emergency fund is a savings account set aside specifically for unexpected expenses.

4. Create a Budget

Budgets are a way to quantify your finances and set realistic goals for where you’d like to be financially. It’s important to create a budget, even if you don’t start following it immediately. Begin by identifying your expenses.

Start by listing all of the things you spend money on, like food, gas, utilities, and insurance. Then, add up all of your expenses. If there are any large expenses, like a car or house payment, put that amount on top of the rest.

Once you have all of your expenses listed, you can create a budget. In your budget, add up all of your income, including salary, social security, pensions, and any other forms of income you have.

Next, you’ll have to figure out where your money is going. You can do this by looking at your list of expenses and figuring out where they are going. For example, if you have a $400 electricity bill, you can figure it out by looking at your expenses list.

A budget helps you plan out how much money you’ll need each month to cover your bills and other expenses.

Start by listing all of your monthly expenses, then add up the total. List any income sources you expect to receive. Finally, subtract the total of your expenses from your expected income. This will give you an idea of what you need to do to reach your desired level of savings.

5. Teach Them About Money Management

It’s important for your child to learn money management skills, even if they aren’t going to be the one doing the spending. One of the most important skills for your child to learn is how to pay bills on time. If your child is going to be responsible for paying the bills, they must learn how to do so on time.

Once you’ve determined how much you need to save each week, start teaching your child about budgeting. Explain why saving money is important, and show them how to use a budget calculator to track their spending among other good financial habits.

Bottom Line

Retirement is a great time in your life as it opens the doors to a period of carefree adventure and relaxation. However, it’s important to be prepared for the transition, especially when it comes to securing your children’s financial security. You can do this by setting up a healthy retirement plan, saving as much as possible, and educating your children about money management.